The government of Pakistan, Finance Division (Regulation Wing) issued a Notification on 03-01-2025 in connection with the Clarification of Voluntary Retirement Penalties and Special Family Pension. The details are as follows:

Clarification Voluntary Retirement Penalties and Special Family Pension

Earlier, the Finance Division issued the Notification of Voluntary Retirement Penalties 2024 for pensioners who retire before the superannuation age, i.e., 60 years. In this Notification, the FD mentioned that if the employee gets retirement before 60 years of age, then he will have to deduct 3% per annum. Now the Finance Division Govt of Pakistan has issued the Notification for its clarification.

As per the Notification, the following the Finance division clarifies for special family pension and voluntary retirement penalties.

Questions and Reply by Finance Division

The queries relate to special family pension and voluntary retirement penalties for the Federal Government pensioners/employees.

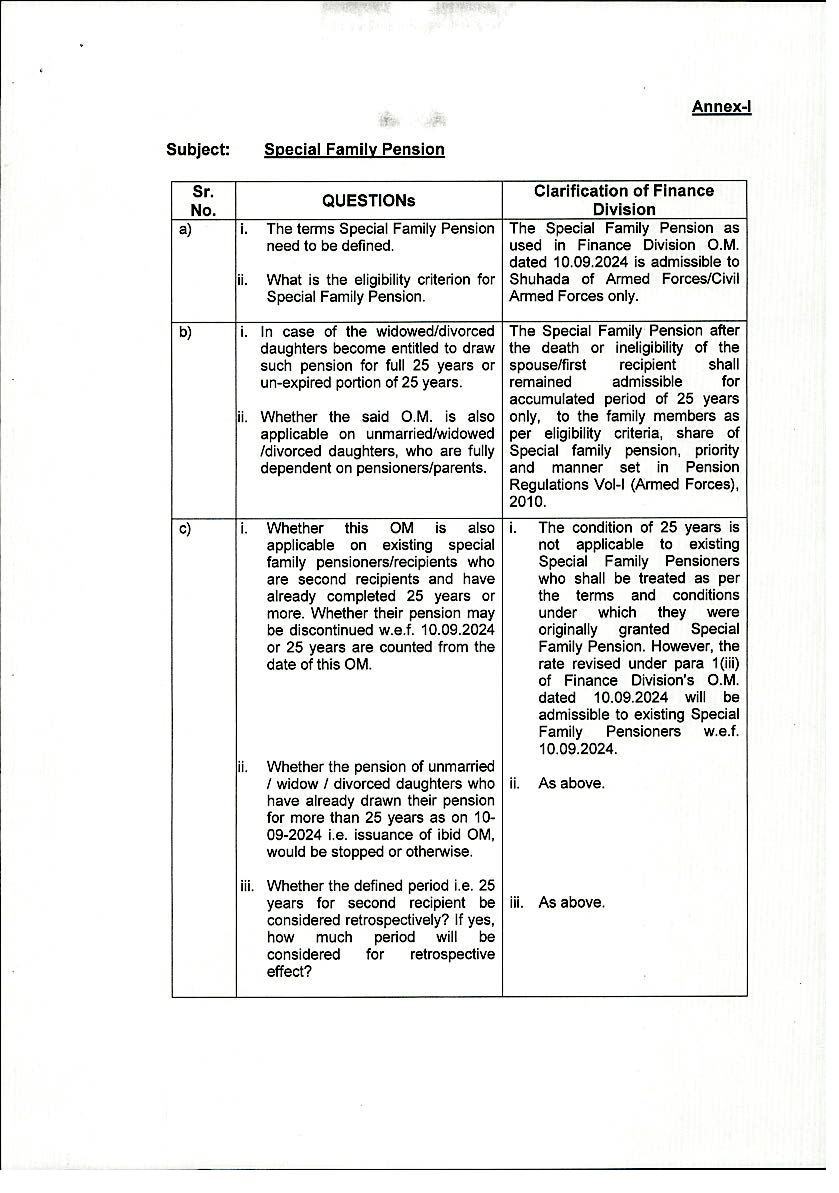

Queries regarding Special Family Pension

| Sr. No. | Questions | Clarification of Finance Division |

| a) | i. The Term Special Family Pension needs to be defined.

ii. What is the eligibility criterion for a special family Pension? |

The Special Family Pension as used in Finance Division O.MN. dated 10.09.2024 is admissible to Shuhada of Armed Forces / Civil Armed Forces only. |

UnExpired Portion of Pension /Unmarried/widowed/divorced daughters

| Sr. No. | Questions | Clarification of Finance Division |

| b) | i. In case of the widowed / Divorced daughters become entitled to draw such pension for the full 25 years or an un-expired portion of 25 years.

ii. Whether the said O.M. is also applicable to unmarried / widowed / divorced daughters, who are fully dependent on pensioners / parents. |

The Special Family Pension after the death or ineligibility of the spouse / first recipient shall remain admissible for an accumulated period of 25 years only, to the family members as per eligibility criteria, the share of Special family pension, priority, and manner set in Pension Regulations Vol-I (Armed Forces), 2010. |

Condition of 25 Years

| Sr. No. | Questions | Clarification of Finance Division |

| c) | i. Whether this OM is also applicable to existing special family pensioners / recipients who are second recipients and have already completed 25 years or more. Whether their pension may be discontinued w.e.f. 10.09.2024 or 25 years are counted from the date of this OM.

ii. Whether the pension of unmarried / widow / divorced daughters who have already drawn their pension for more than 25 years as of 10-09-2024 i.e. issuance of ibid OM, would be stopped or otherwise. iii. Whether the defined period i.e. 25 years for the second receipt be considered retrospectively? If yes, how much period will be considered for retrospective effect?

|

i. The condition of 25 years does not apply to existing Special Family Pensioners who shall be treated as per the terms and conditions under which they were originally granted Special Family Pension. However, the rate revised under para 1 (iii) of the Finance Division’s O.M. dated 10.09.2024 will be admissible to existing Special Family Pensioners w.e.f. 10.09.2024.

ii. As Above

iii. As Above |

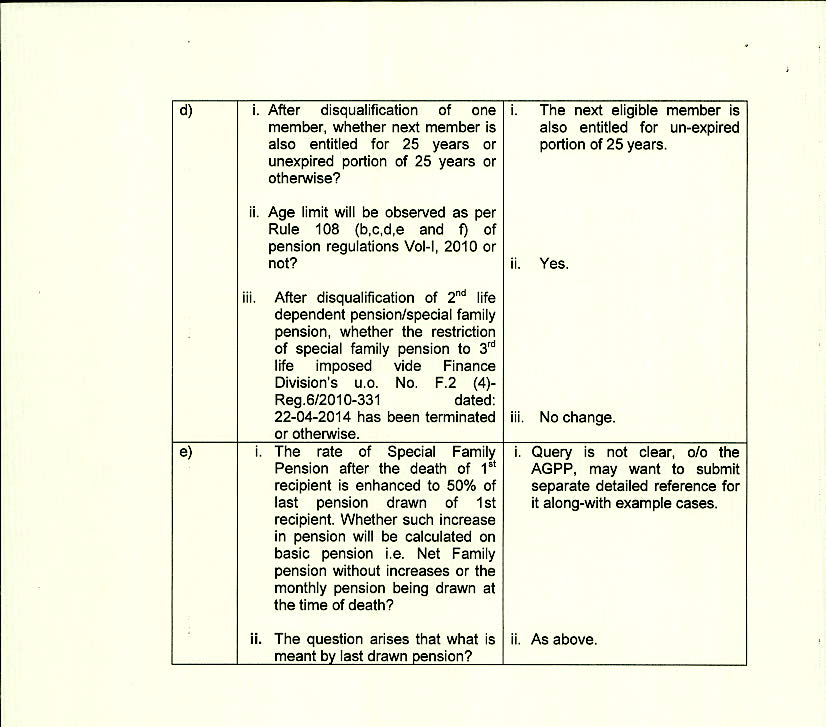

Next Member and Entitlement 25 Years

| Sr. No. | Questions | Clarification of Finance Division |

| d) | i. After the disqualification of a new member, whether next member is also entitled to 25 years or an unexpired portion of 25 years or otherwise?

ii. Age limit will be observed as per Rule 108 (b,c,d,e, and f) of pension regulations Vol-I, 2010 or not? iii. After the disqualification of 2nd life dependent pension ? special family pension, whether the restriction of special family pension to 3rd life imposed vide Finance Division’s u.o No. F.2 (4)- Reg.6/2010-331 dated: 22-04-2014 has been terminated or otherwise. |

i. The next eligible member is also entitled to an un-expired portion of 25 years.

ii. Yes.

iii. No change. |

Rate of Special Family Pension

| Sr. No. | Questions | Clarification of Finance Division |

| e) | i. The rate of Special Family Pension after the death of the 1st receipt is enhanced to 50% of the last pension drawn of the 1st receipt. Whether such increase in pension drawn of 1st receipt. Whether such an increase in pension be calculated on basic pension i.e. Net Family pension without increases or the monthly pension being drawn at the time of death?

ii. The question arises what is meant by the last drawn pension? |

i. Query is not clear, o/o the AGPP, may want to submit a separate detailed reference for it along with example cases.

ii. |

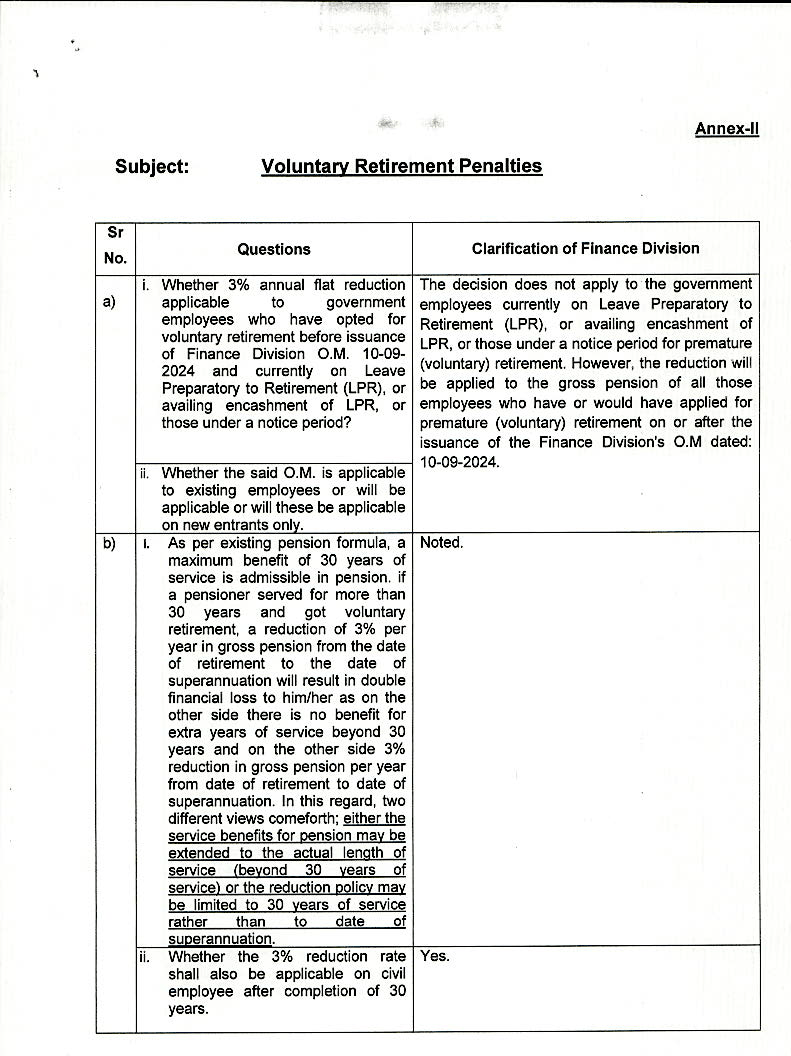

Voluntary Retirement Penalties

| Sr. No. | Questions | Clarification of Finance Division |

| a) | i. Whether a 3% annual flat reduction applies to government employees who have opted for voluntary retirement before issuance of Finance Division O.M. 10-09-2024 and are currently on Leave Preparatory to Retirement (LPR), or availing encashment of LPR, or those under a notice period?

ii. Whether the said O.M. applies to existing employees or will be applicable or will be applicable to new entrants only. |

The Decision does not apply to government employees currently on Leave Preparatory to Retirement (LPR), or availing encashment of LPR, or those under a notice period for premature (voluntary) retirement. However, the reduction will be applied to the gross pension of all those employees who have or would have applied for premature (Voluntary) retirement on or after the issuance of the Finance Division’s O.M. dated: 10-09-2024. |

Beyond 30 Years of Service / Panelity

| Sr. No. | Questions | Clarification of Finance Division |

| b) | i. As per the existing pension formula, a maximum benefit of 30 years of service is admissible in pension. If a pensioner served for more than 30 years and got voluntary retirement, a reduction of 3% per year in gross pension from the date of retirement to the date of superannuation will result in double financial loss to him/her as on the other side there is no benefit for extra years of service beyond 30 years and on the other side 3% reduction in gross pension per year from date of retirement to date of superannuation. In this regard, two different views come forth; either the service benefits for pension may be extended to the actual length of service (beyond 30 years of service) or the reduction policy may be limited to 30 years of service rather than to the date of superannuation.

ii. Whether the 3% reduction rate shall also be applicable to civil employees after the completion of 30 years. |

i. Noted.

ii. Yes. |

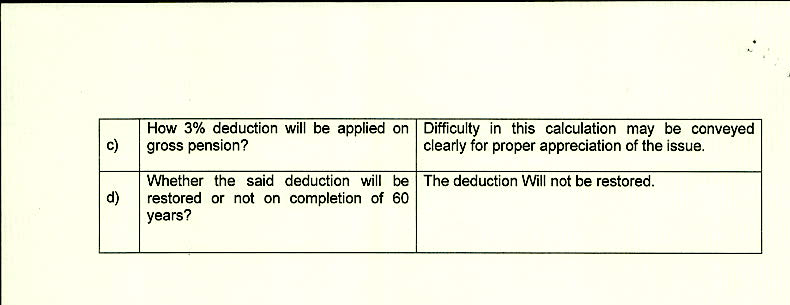

3% Deduction and Gross Pension

| Sr. No. | Questions | Clarification of Finance Division |

| c) | How 3% deduction will be applied to a gross pension? | Difficulty in this calculation may be conveyed clearly for proper appreciation of the issue. |

Restoration of 3% Deduction

| Sr. No. | Questions | Clarification of Finance Division |

| d) | Whether the said deduction will be restored or not on completion of 60 years? | The deduction will not be restored. |

")