The Government of Pakistan, Finance Division, issued a Notification on 04-03-2025 in connection with the clarification Calculation of Emoluments and Future Pension Increase Policy 2025 for Retired Employees. Future Pension Increase Policy will impact retirees from January 1, 2025, as per government regulations. The Finance Division’s latest notification explains the calculation of net pension increases, family pensions, and baseline pensions. This guide provides clarity on the new pension structure for future retirees.

Clarification Calculation of Emoluments and Future Pension Increase Policy 2025 for Retired Employees

As per the Notification No. F. 9(3)/Reg.6/2024-264 of Finance Division (Regulations Wing) dated 4th March 2025, the FD issued the clarification for pension calculation and increase in pension in the future. There are the following aspects that the Finance Division clarified:

- Calculation of Emoluments for Pension

- Multiple Pensions

- Future Increase Methodology in Pension

The Finance Division’s O.Ms. No. F. 9(3)R-6/2024-401 to 403, dated 01.01.2025, reference the above subject(s). Various quarters have raised queries seeking necessary clarification. The responses to those queries are provided in attached Annex-I, Annex-II, and Annex-III for information and necessary implementation of all, please.

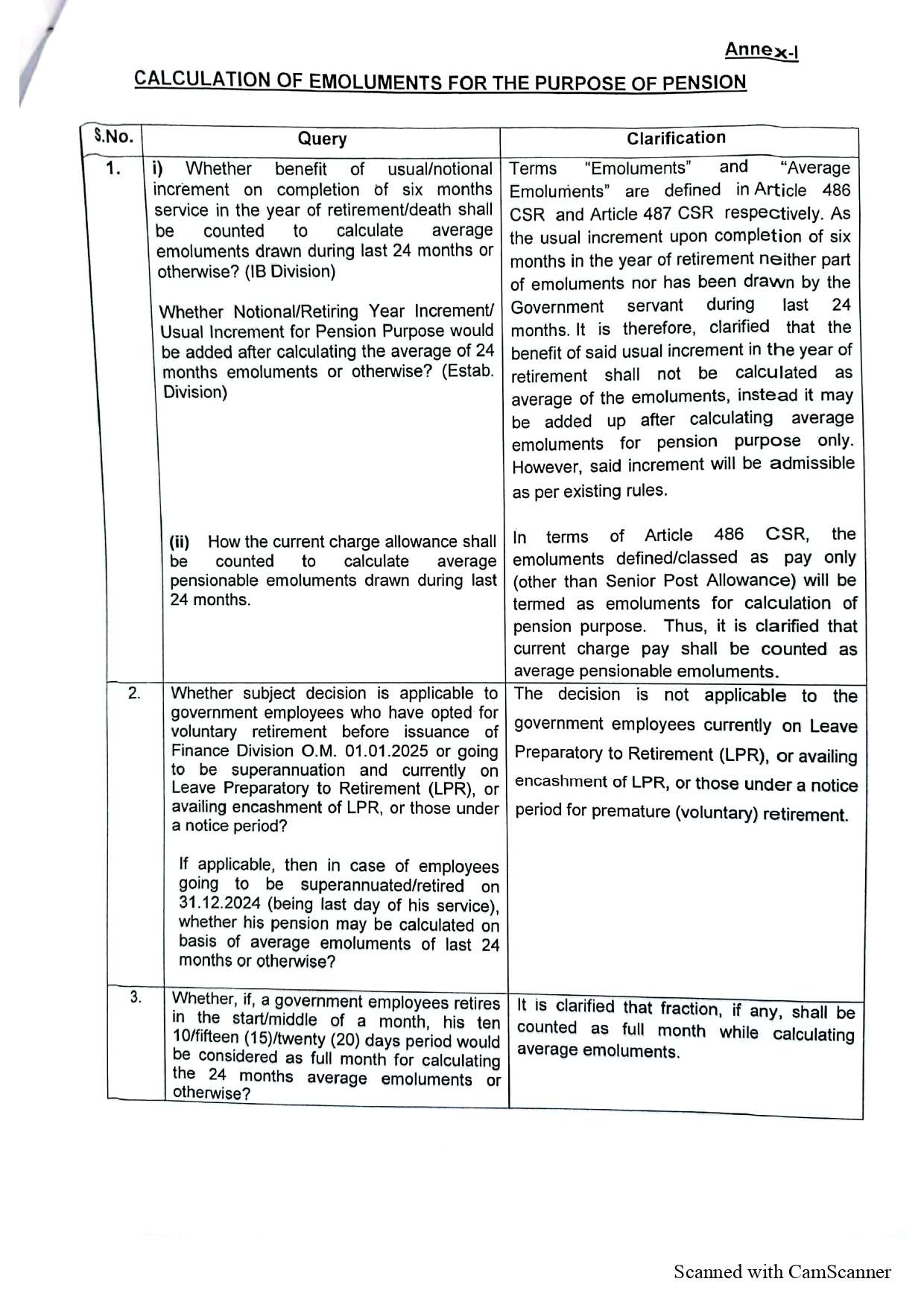

Annex-I

Calculation of Emoluments for Pension

| S. No. | Query | Clarification |

| 1. |

(i) Should the benefit of the usual/notional increment, earned after completing six months of service in the year of retirement or death, count toward calculating the average emoluments drawn during the last 24 months? (IB Division) Should the calculation of the 24-month average emoluments exclude the Notional/Retiring Year Increment/Usual Increment for pension purposes, and should it be added separately afterward? (Estab. Division) |

Articles 486 CSR and 487 CSR define the terms “Emoluments” and “Average Emoluments,” respectively. Since the Government servant does not draw the usual increment upon completing six months in the year of retirement during the last 24 months, it does not form part of the emoluments and does not count toward the calculation of average emoluments. Instead, the calculation should include it after determining the average emoluments for pension purposes only. However, the existing rules continue to allow this increment. |

| (ii) How the current charge allowance shall be counted to calculate average pensionable emoluments drawn during the last 24 months. | In terms of Article 486 CSR, the emoluments defined/classed as pay only (other than Senior Post Allowance) will be termed as emoluments for the calculation of pension purpose. Thus, it is clarified that the current charge pay shall be counted as average pensionable emoluments. | |

| 2. | The subject decision applies to government employees who have opted for voluntary retirement before issuance of Finance Division O.M. 01.01.2025 or going to be superannuation and currently on Leave Preparatory to Retirement (LPR), or availing encashment of LPR, or those under a notice period.

If applicable, then in case of employees going to be superannuated/retired on 31.12.2024 (being the last day of his service), whether his pension may be calculated based on average emoluments of the last 24 months or otherwise? |

The decision does not apply to the government employees currently on Leave Preparatory to Retirement (LPR), availing encashment of LPR, or those under a notice period for premature (voluntary) retirement. |

| 3. | If a government employee retires at the start or middle of a month, the 10-, 15-, or 20-day period will not count as a full month when calculating the 24-month average emoluments. Instead, only completed months will be considered under the applicable rules. | It is clarified that a fraction, if any, shall be counted as a full month while calculating average emoluments. |

Annex-II

Multiple Pensions

| S. No. | Query | Clarification |

| 1. | Does the condition to opt for one pension apply to those who have already been drawing more than one pension before the issuance of said O.M. or otherwise? | No. The decision is not applicable to Federal Government employees who are drawing multiple pensions prior to issuance of O.M. F.No.9(3)R-6/2024-402 dated 01.01.2025 on the subject. However, Government employees re-employed on or after 01.01.2025 must adhere to the condition of opting for one pension. |

| (ii) Whether the condition to opt for one pension applies to both self and family pension or otherwise? | The point was already defined in sub-para (ii) of O.M. F. No. 9(3)R.6/2024-402 dated: 01.01.2025 on the subject. |

Annex-III

FUTURE INCREASE METHODOLOGY IN PENSION

| S. No. | Query | Clarification |

| 1. | Whether the increases (15%-2011, 7.5% – 2015, 15% -2022, 17.5%-2023 and 15%-2024) granted “Net Pension + Increases” to the existing pensioners from time to time by the Federal Government would also be admissible to the employees retiring on or after 01.01.2025 as per policy in vogue or otherwise? | The Finance Division’s O.M. F. No. 9(3)R-6/2024-403, dated 01.01.2025, outlines the calculation methodology for future increases that the Government will announce. Pensioners who retired on or after 01.01.2025 should calculate the existing increases of 2011, 2015, 2022, 2023, and 2024 based on existing practice until further orders.. However, the baseline pension shall be the Gross pension minus the commuted portion as given in sub-para (a) of the O.M. ibid. |

| 2 | Will the family pension of existing pensioners who pass away on or after 01.01.2025 be granted to the widow at 75% of the Net Pension or 75% of the baseline pension (as drawn on 31.12.2024)? | Family Pension shall be calculated on the basis of pension being drawn and not the baseline. The pension so calculated shall become the baseline pension for further increases. |

| 3. | What would be the baseline pension of existing pensioners whose commuted portion of pension will be restored on or after 01.01.2025? |

|

Download Full Notification